Dive Brief:

- Red Lobster has been struggling to pay its bills on time for several months, according to commentary from Ragini Bhalla, head of brand and spokesperson for Creditsafe, emailed to Restaurant Dive.

- In October, about 70% of the chain’s bills were late, with a bulk (37%) 31 to 60 days late and over 9% were over 91 days late. By February, 25% of its bills were paid on time and over half were paid 61 to 90 days late, according to Creditsafe data.

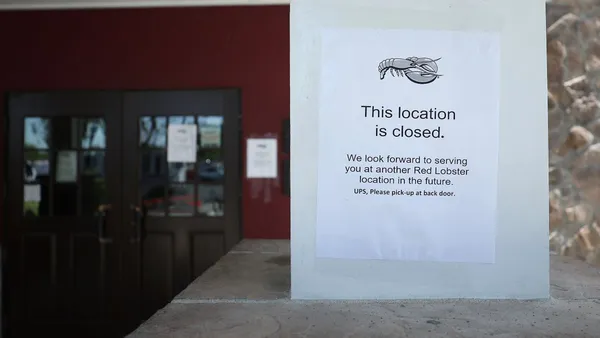

- This report of financial troubles comes amid the chain’s appointment of a restructuring expert as its new CEO and rumors that it could be heading toward bankruptcy.

Dive Insight:

Given the chain’s mounting losses, Red Lobster will likely continue to struggle to pay its bills. One of the top reasons for losses it generated last year was from its Endless Shrimp promotion, which changed from once a week to every day. That promotion was so popular that it ended up costing the company $11 million during Q3 2023, Bhalla noted. Losses continued last year, with the chain reporting $12.5 million in operating revenue loss during Q4 2023.

Red Lobster’s Days Beyond Terms, or the average days a firm pays its bills past the invoice date, are increasingly worrisome, Bhalla said. In December, the chain’s DBT was 15, which more than doubled by February at 47. As of March, the chain averages 48 days to pay its suppliers past payment terms, Bhalla said.

“It’s also worrying that the company’s DBT has been so volatile and spiked drastically multiple times,” Bhalla said. “This shows the company may not have done the necessary cash flow forecasting to protect itself from potential losses, revenue declines and challenging market conditions. It probably doesn’t help that Thai Union Group has now decided to exit from its investment in Red Lobster.”

Thai Union Group earlier this year said it would divest its holdings in Red Lobster due to ongoing losses that were negatively impacting the company. It originally bought a 25% stake in the company for $575 million in 2016. The company led an investment group that bought the remaining stake from Golden Gate Capital in 2020.

If Red Lobster ends up filing for bankruptcy, it could help “alleviate pressures from high rent and labor costs,” Sarah Foss, global head of legal at Debtwire, wrote in an email to Restaurant Dive. Foss added that Red Lobster would be the first major restaurant chain to declare bankruptcy this year, when retailers and a large number of healthcare and telecommunications firms have filed for Chapter 11 bankruptcy.

“Chapter 11 can be a useful tool for a restaurant or retail chain facing financial distress as it allows a debtor to renegotiate and reject burdensome leases and contracts, which are often a major financial strain on a distressed company in these sectors,” Foss said. “Although Red Lobster’s path through bankruptcy is unclear, the company … is likely considering both a sale as well as its standalone restructuring options.”

Red Lobster didn’t immediately respond to a request for comment.